ACTIVIST VC BLOG

The Danger of M&A Imbalance

October 26, 2018This week we continue analyzing the recent startup M&A study by our friends at Mind the Bridge. Now we focus on the tech startup M&A balance in different geographies.

The Great Importance of Tech Startups

In the US, tech startups have made a major impact on the economy. Out of the Fortune 500 companies in the 1950s, nearly 90% have been pushed out by new growth companies, the majority of them VC-funded. Massive Creative Destruction fueled by VC funding:

- VC-backed public companies account for 20% of the total public market value and 44% of the R&D spending in the US

- Seven of the ten most valuable companies in the world have VC background

So – where’s the problem?

European (and Finnish) VCs are often criticized selling their portfolio companies too early: most of the value growth is reaped by the new owners. The buyers are almost invariably foreign – and most often from the US.

Let’s have a look at the data:

- The US has a bit more acquisitions than exits

- Europe has more exits compared to acquisitions

- Rest of the world, in general, is a heavy net seller of startups

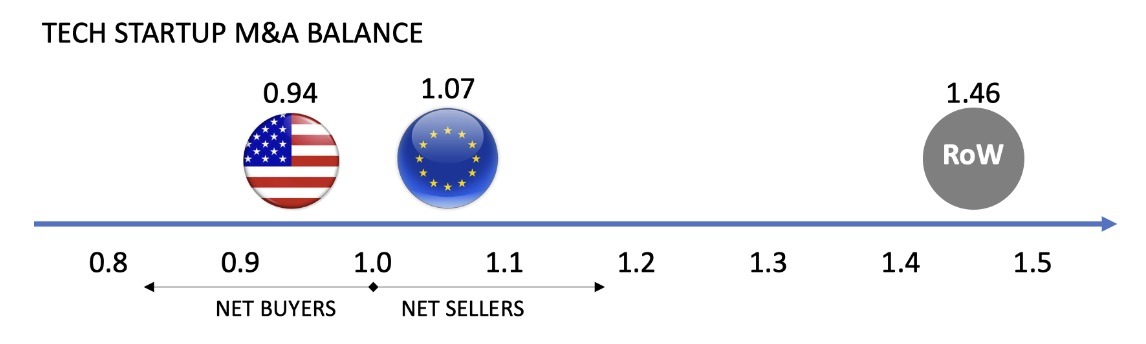

The Global M&A Balance: Net Buyers and Net Sellers

In other words, the US sells a bit fewer technology startups than it acquires, the ratio is 0,94. The US also creates more value out of the startups they sell: median exit price is $100m, for European startups the median is only $30m.

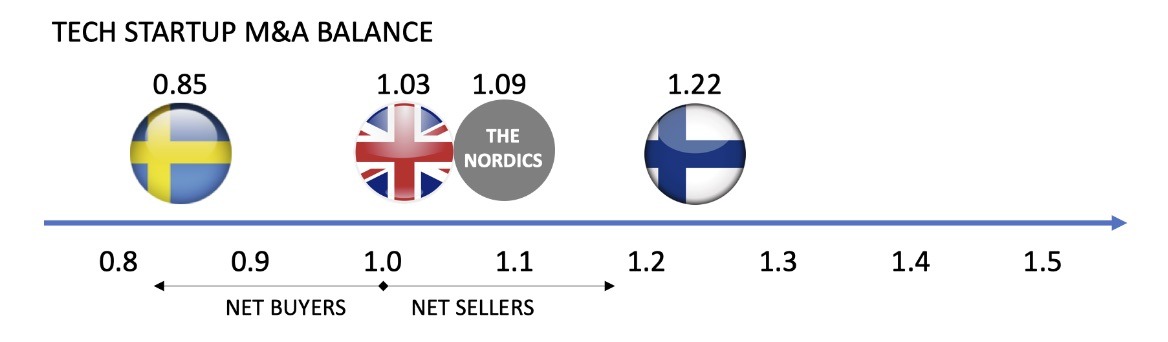

In Europe, the UK has an M&A balance ratio of 1.03 which is slightly better than the rest of Europe. The Nordics have an overall ratio of 1.09 which is very close to the European average. The ratio for Finland (1.22) is well above the European average.

In the European context, Finland is exit-heavy:

we sell startups with a ratio of 1.22

Why does this matter?

Can an economy flourish in the long term by employing the Israeli model – exporting 2.1 times more tech startups than acquiring?

Or would it make sense to focus on creating a stronger domestic industry that can also acquire the best available innovations to fuel growth? This sounds like a safer long-term strategy.

The US could be a benchmark. The US market is full of professional serial tech buyers – companies that are “outsourcing” a significant part of their R&D to fast-moving VC-funded startups. They let the nimble startups develop new technology and then acquire the companies to leverage the innovations with their own superior distribution power. For a breakdown of the most active buyers (18 of the top 20 are US-based).

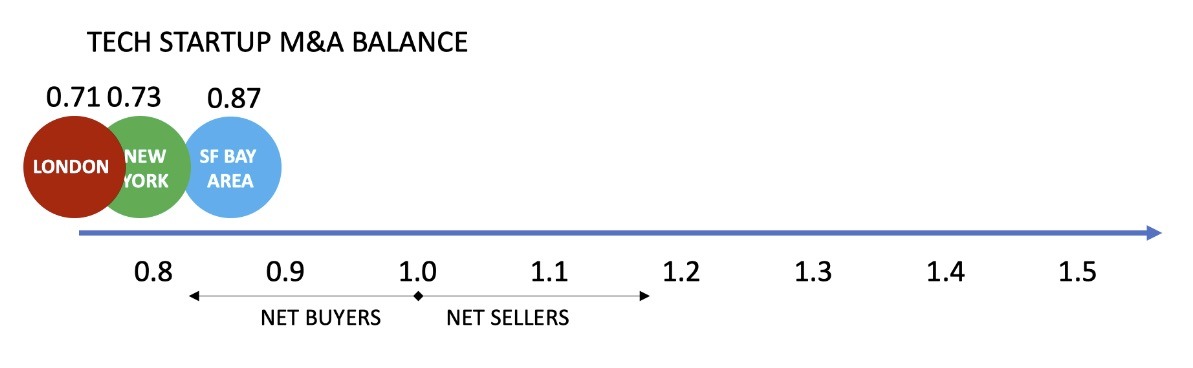

Another data point – there are three business hubs that sell a huge amount of start-ups: SF Bay Area, New York, and London. They create 23% of the global tech startup exit volume. But they dominate the world even more on the buy side: they represent 30% of the global tech startup acquisitions!

All the three key startup hubs are also very strong net buyers of tech startups

These super hubs support the idea that high tech business thrives in tight clusters in which a critical mass of success factors are created. These hubs have also developed the culture and processes to acquire expertise and innovations from the outside – as opposed to not-invented-here…

The Nexit take

At Nexit we believe it is important for the development and renewal of European economies to:

- Create a steady stream of world-class innovative startups

Some startups will have the power to stay independent and become new industry giants. Some will be bought domestically. But for the majority, the best possible buyer is from abroad. - Use tech startup M&A to renew faster and be more agile

The global competition is getting fiercer at an accelerating pace – it is increasingly difficult to respond to these challenges with internal measures only.

There seems to be much room for development in these two areas – both in Finland and more generally in most European countries:

1. European startups are sometimes sold too early

The low median exit valuation of European startups ($30m vs. $100m for US startups) underlines the problem. Areas for improvement:

- We need stronger and larger VC funds with perseverance and long-term thinking to push startups to higher exit valuations.

- More IPOs are needed to create stronger domestic industries – well funded public companies that are large enough to make meaningful acquisitions.

2. Big industrials in Finland don’t use enough M&A

The Finnish tech startup M&A Imbalance is indicating a lack of industry M&A activity. Statistics strongly suggest that big corporations with the size and resources sufficient for M&A are not reacting strongly enough to the accelerating change and digitalization.

Are the majority of top twenty Finnish corporations suffering from the not-invented-here syndrome or are they just gun-shy?

Prof Alberto Onetti, the author of our source study, says: “The common wisdom is that acquisitions have played a central role in Silicon Valley’s success – buying startups is one of the fastest ways for companies to embrace disruption and keep innovating.”

These are wise words that we agree with wholeheartedly.

WE'D LOVE TO HEAR YOUR COMMENTS